Our Perspectives on Recent Market Volatility

Key Points:

During the last three months of 2018, stock markets around the world have sold off as investors have become increasingly apprehensive about a global economic slowdown and rising interest rates in the U.S.

A lot changed since 2017, including a shift from synchronized growth across economies around the world to divergent growth, and a significant shift higher in U.S. interest rates.

It is still expected that overall global economic growth, albeit lower, will likely still be positive in 2019 and that the U.S. Federal Open Market Committee will probably be very deliberate about raising rates further.

Investors that have properly balanced and diversified portfolios should not worry excessively about stock market volatility. Sticking to one’s investment plan during times like this can increase the chance of achieving investment success and substantially growing wealth over time.

What Happened in the Markets and Why

During the last three months of 2018, stock markets around the world sold off as investors became increasingly apprehensive about a global economic slowdown. Concerns about a slowdown actually started earlier in the year. Tariffs and threats of such slowed international trade, impacting China and Europe. Meanwhile, unfavorable currency movements hurt emerging market countries across the board that are heavily dependent on imports, exports, and international investment. More recently, investors are concerned that the slowdown is spreading and might eventually hurt the U.S. economy.

On top of growth concerns, investors became increasingly nervous about rising interest rates in the U.S. Investor anxiety about interest rate policy is increasingly focused on whether the U.S. Federal Open Market Committee (FOMC) has increased rates too much, and how much higher the FOMC plans to go. As expected, the FOMC raised interest rates again in December signaling their continued confidence in the strength of the U.S. economy. However, they also pared back some of their projections for both interest rate increases and economic growth in 2019 and beyond.

How and Why the Story Has Changed

In 2017, all 45 of the world’s major economies grew in sync for the first time in a decade, according to the Organization for Economic Cooperation and Development (OECD). It is safe to say that things on the economic front have changed significantly in a matter of 12 months. European and Chinese economic expansions have slowed. There are many things that have contributed to their recent slowdown including global trade friction, geopolitical tensions in the 19-country Eurozone, and uncertainty around the U.K.’s departure (Brexit) from the European Union.

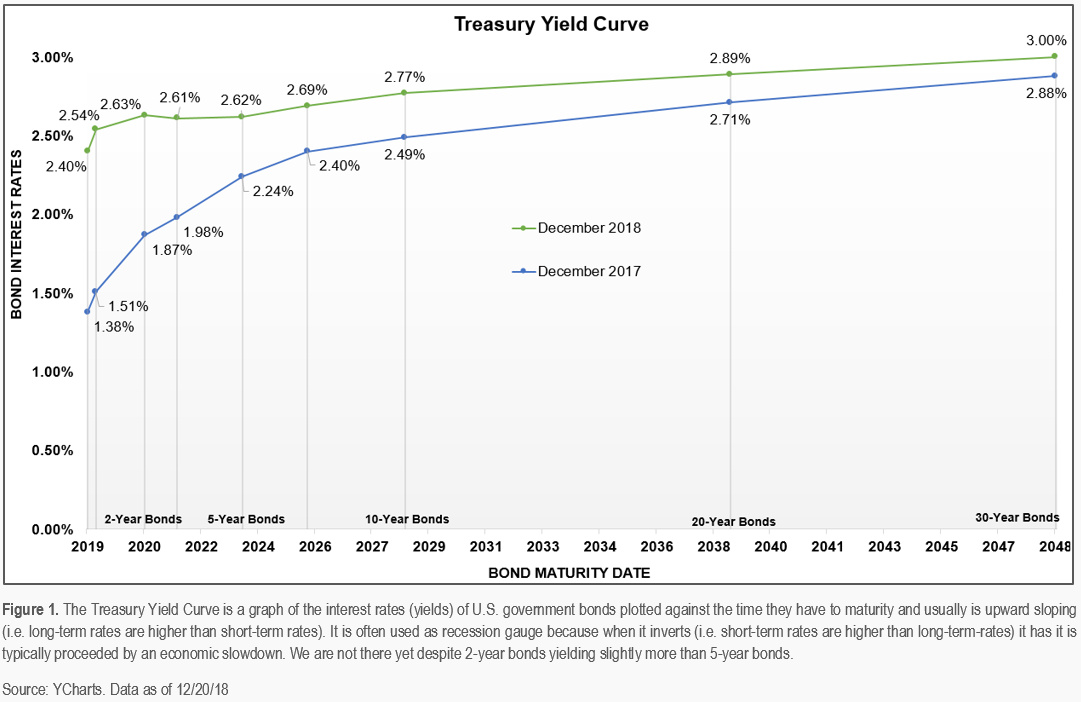

Similarly, the interest rate story in the U.S. was markedly different in 2018 compared to the prior year. In 2017, U.S. rates were significantly lower than they are now, and the U.S. treasury yield-curve, often used as a recession gauge, was more “upward sloping” than it is now. (See Figure 1.) The reason for the change in the interest rate story is more obvious. The FOMC raised short-term rates four times in 2018 (impacting the short-term end of the curve), while U.S. growth and inflation rates increased (impacting the long-term end of the curve). The FOMC raising interest rates isn’t generally a problem because it means that the U.S. economy is improving. However, investors become concerned when the FOMC raises rates too much and too fast, which has historically caused recessions.

Our Thoughts About All This

Although economic fundamentals abroad weakened in 2018 with some countries like Germany and Italy experiencing negative growth in the third quarter, it is still expected that overall global economic growth, albeit lower, will likely still be positive in 2019. There are two key reasons why this is likely to happen. The first is that the U.S. economy, the largest in the world, is healthy and is expected to continue growing at a relatively robust rate. The second is that central banks around the world remain patient and accommodative by keeping interest rates low and, especially in the case of China, remain ready to provide additional economic stimulus if needed.

High interest rates are generally not good for an economy because it tends to tighten financial conditions that typically result in a slowdown in business investment, consumer spending, and sometimes a country’s export market. However, higher interest rates in the U.S. have thus far not significantly impacted the U.S. economy. Solid economic and corporate fundamentals combined with tax cuts and new Federal spending has resulted in a pickup in growth rather than a slowdown. In other words, the U.S. has been able to withstand current rate levels.

Going forward, the FOMC expects two rate hikes in 2019, down from three, while indirectly signaling that they would pause if warranted by incoming data. This is an indication that the FOMC is likely going to be very deliberate about raising rates further and that they are closer to the end. Given this stance, it is not likely that the FOMC will raise rates quickly and to the point that it tips the U.S. economy into a recession any time soon. With that said, if the yield curve were to flatten more, or invert, it would indicate that the U.S. economy is going to slow down at some point in the future (historically anywhere between around 6 and 36 months later). However, given current solid corporate and economic fundamentals, and a stock market that is not excessively overheated, it is likely that a slowdown would be relatively modest and brief, not like 2008.

Markets Environment in 2019 and Beyond

Like 2018, stock market volatility will likely remain elevated in 2019 because unfortunately, improvements with tariffs and trade tensions are not expected any time soon. Additionally, geopolitical news and events will likely continue to weigh on stock markets and could drive big swings due to investor uncertainty and speculation. Although uncertainty about U.S. interest rate policy will remain, a more patient and data-driven FOMC could help ease investor concerns about the U.S. tipping into a recession.

A global recession is not expected in 2019. Despite the recent slowdown in global growth, growth overall, is still positive, corporate fundamentals are strong, and accommodative monetary policy broadly remains in place. Stock markets could return to positive territory in 2019, especially after the healthy pullback in 2018, following a year with double-digit returns across most stock asset classes. However, given where we are in the economic cycle, returns are likely to be lower over the next few years relative to what they’ve been over the last several years of the recovery.

What Investors Should Do

Investors that have properly balanced and diversified portfolios should not worry excessively about stock market volatility. The recent declines are a natural part of the stock market, and it is why over long periods, stocks typically generate higher returns than more conservative investments like bonds. However, the recent market declines prove how bonds serve an essential purpose in a balanced portfolio.

Having “balance” in a portfolio means having an appropriate amount of high-quality bonds to complement stocks. This can help to ensure that an investor will be able to ride the stock market wave up and down without eventually feeling the need to get out of the market to sleep at night. High-quality bonds have been a strong ballast in portfolios over the last three months and should continue to provide support during future bouts of market volatility.

Times like this give investors the opportunity to “rebalance” their portfolio by trimming from bonds that have appreciated and adding to stocks that have gone down significantly. It also gives taxable investors the opportunity to “harvest” investment losses to reduce taxes by offsetting other investment gains and some ordinary income. Rebalancing and tax-loss-harvesting is something we regularly do at Capstone for clients.

One of the principals of our philosophy is that most investors should stay invested for as long as possible. Our philosophy is contrary to an approach that suggests that one should try to “time the market” by getting out when markets conditions get bad and buying back in later. Although this approach sounds logical, in practice, it is tough to get right more times than not and can often result in missing out on significant returns during recovery periods.

Market timing is not an enduring investment strategy. The enduring strategy is staying invested in a properly balanced and diversified portfolio, and implementing a disciplined investment process. Sticking to one’s investment plan during times like this can increase the chance of achieving investment success and substantially growing wealth over time.

Disclosures

Please remember that different types of investments involve varying degrees of risk, including the loss of money invested. Past performance may not be indicative of future results. Therefore, it should not be assumed that future performance of any specific investment or investment strategy, including the investments or investment strategies recommended or undertaken by Capstone Financial Advisors, Inc. (“Capstone”) will be profitable. Definitions of any indices listed herein are available upon request. Please contact Capstone if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and services, or if you wish to impose, add, or modify any reasonable restrictions to our investment management services. This article is not a substitute for personalized advice from Capstone and nothing contained in this presentation is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. Investment decisions should always be based on the investor’s specific financial needs, objectives, goals, time horizon, and risk tolerance. This article is current only as of the date on which it was sent. The statements and opinions expressed are, however, subject to change without notice based on market and other conditions and may differ from opinions expressed by other businesses and activities of Capstone. Descriptions of Capstone’s process and strategies are based on general practice, and we may make exceptions in specific cases. A copy of our current written disclosure statement discussing our advisory services and fees is available for your review upon request.