A Tax-Smart Way to Give More

Key Points:

Donor-advised funds have become popular in recent years, in part because they are easy to establish and relatively inexpensive to maintain.

The primary benefit of a donor-advised fund is that it allows an individual to donate assets to a charity today and receive an immediate tax deduction even though the actual contribution is not distributed to the charity until a later date.

When used correctly, a donor-advised fund can be a powerful charitable planning vehicle that may increase the total amount donated to charity, while providing tax benefits to the donor.

VIEW A SHORT SUMMARY VIDEO

For most individuals, the main goal of giving to charity is not necessarily to take advantage of the income tax deduction or to receive some benefit in return, but rather to support an organization that has a mission they believe in. When deciding when and how to give to charity, it should ultimately come down to personal preference. Although most people are happy simply writing a check to their favorite organization, there are more tax efficient ways to donate that may also increase the benefit received by the charity. One such strategy that can help maximize charitable contributions is using a “donor-advised fund.”

What is a donor-advised fund?

A donor-advised fund (DAF) is a charitable account set up specifically for the donation of cash or other assets, ear-marked to be donated to a qualifying charity. A donor contributes to the DAF, which is managed by a custodian, and receives an immediate tax deduction for the value of the amount contributed to the account. Later, even during subsequent taxable years, the donor can then direct the DAF to make grants to qualifying charities of their choice.

Donor-advised funds have become popular in recent years because they provide donors with a much simpler and less expensive alternative to setting up a private foundation. The timing of the actual donation to charity is also more flexible, and most DAFs provide online donation and grant capabilities as well. Additionally, a DAF gives you the added benefit of confidentiality, if desired.¹

What are the benefits of a DAF and how does it work?

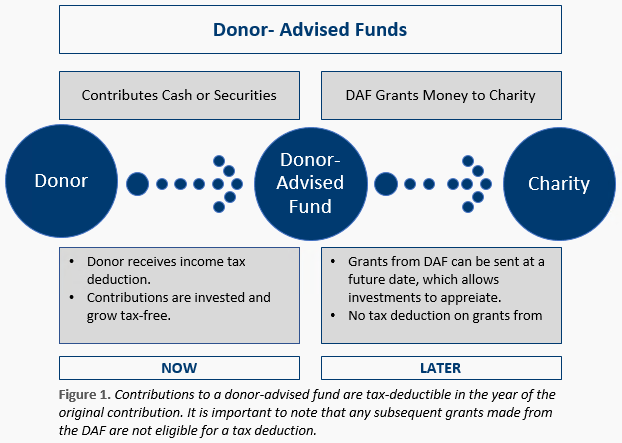

A key characteristic of a DAF is that it allows someone to donate assets to charity today and receive an immediate tax deduction, even though the actual funds may not be granted to a charity until some point in the future. This provides a timing benefit that is not available for outright gifts to charity. This timing benefit can be helpful if a donor has not yet committed to a particular charity, or would like to maximize the tax benefit from a donation. For example, individuals can “front-load” their contributions to a DAF in years that they have higher levels of income, or are subject to higher tax rates.² This typically occurs when someone receives a large bonus, exercises stock options, or sells a business. Since the amount you can deduct as a charitable contribution is limited by your adjusted gross income (AGI), it would be more beneficial, from a tax perspective, for the donor to donate in years when they have a higher AGI.

The timing benefit is also important when considering itemized deduction levels. With the changes included in the Tax Cuts and Jobs Act, and the increase in the standard deduction, bunching donations into one year to exceed the standard deduction in that year may provide a higher tax benefit overall. See Figure 1, for a general overview of the basic mechanics of a DAF.

In addition to the timing benefits, DAFs can also be helpful to manage charitable activity. The custodians of most DAFs provide recordkeeping, acknowledgements to charities and online capabilities that might not be available when working directly with a charity.

Should I contribute cash or stock to a Donor-Advised Fund?

Another benefit to setting up a DAF is that it can serve as a conduit for appreciated securities (e.g., stocks).² The situation may arise where an individual wants to take advantage of donating appreciated securities to a charity, but the charity cannot directly receive in-kind donations of this type. If this is the case, the individual could establish a DAF and contribute their appreciated securities to the DAF. The stock would then be sold, and a cash grant distributed to the desired charity.

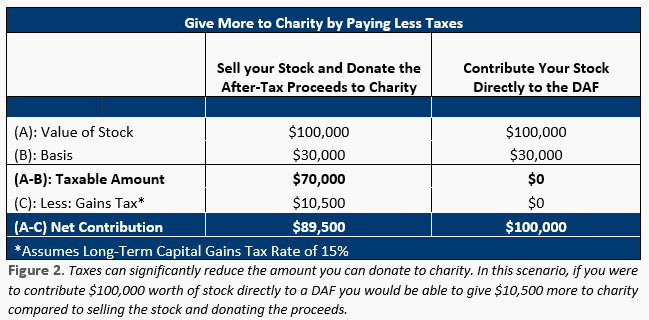

Donating appreciated securities is a powerful planning technique we often recommend to our clients. In addition to the charitable donation, it also provides a tax benefit through the avoidance of tax on long-term capital gains that would otherwise be recognized on the sale of those securities. (Note: Tax on short-term gains cannot be avoided with a DAF.) Since a DAF is treated as a charitable entity, any direct contributions will not create a taxable event to the donor.³ Because of this tax benefit, net contributions to the desired charity may also be increased when using a DAF. As Figure 2 illustrates, by avoiding capital gains tax on a contribution of long-term appreciated securities to a DAF, the charity will ultimately receive a larger donation.

Summary

The decision on whether to utilize a DAF is relatively straight-forward. A DAF is a great tool to use anytime there is a desire to take advantage of an immediate charitable deduction, while making grants to a charity at some later point in time. This strategy works particularly well to provide ease in administration of charitable gifts, timing benefits for grants, and additional potential tax savings. If you have any questions or are considering establishing a DAF, please contact Capstone Financial Advisors to determine if this is the best vehicle to help you reach your charitable goals.

Sources

¹National Philanthropic Trust, DAF vs. Foundation

²Michael Kitces, Rules Strategies and Tactics When Using Donor Advised Funds for Charitable Giving

³Investopedia, Donor Advised Funds Tax Efficient Giving