Important Things to Know About Your Equity Compensation Plan

Key Points:

Equity compensation plans have become increasingly complex for ordinary individuals to understand.

Stock options, Restricted Stock Units, and Performance Shares are the most common forms of equity compensation plans in the United States.

It is important to consider the risk, reward, and tax implications of your compensation packages to make a sound financial decision.

Pharmaceutical giant, Pfizer, introduced equity compensation to corporate America in the early 1950s, and it wasn’t long before other major corporations adopted their own forms of this type of employee benefit. Equity compensation is a means by which a company rewards its employees with ownership in the business. This is often done to attract and retain talent within the company, with the equity compensation typically offered as part of a ‘package’ and rarely as the sole means of compensation.

Equity compensation packages have become increasingly complex for individuals to understand, largely because there are many different forms, each with its own set of risks, rewards, and tax implications. It is important to consider each of these factors to make sound financial decisions. While there are many different forms, more common plans include Non-Qualified Stock Options, Restricted Stock Units, and Performance Shares (or Units).

Non-Qualified Stock Options

Generally, Non-Qualified Stock Options (NSOs) give you the ‘option’ to purchase a stock in the future, for a predetermined price. The options are usually subject to a vesting schedule, which restricts you from exercising your right to purchase the shares until after a specified number of years.

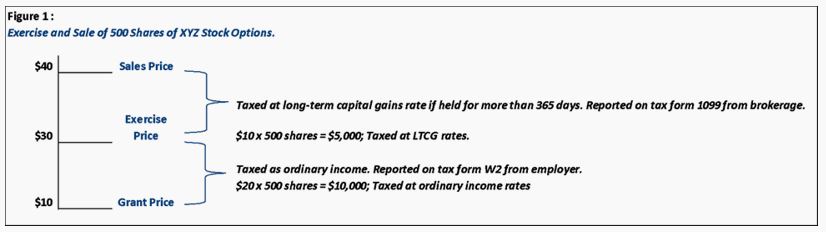

For example, suppose your employer grants you options that will give you the right to purchase 500 shares of the company’s XYZ stock in the future at the stock’s current fair-market-price of $10 per share, often referred to as the grant price. The “intrinsic value” of the options (or the amount of profit that exists in an options contract) on dayone would be $0, because the grant price is equal to the XYZ’s current fair-market-price ($10). However, assume 10 years pass, the options are vested, and the value per share of XYZ stock is now at $30. At this point, you could exercise your option to purchase the stock at the original price of $10. This means you would pay $5,000 to purchase shares that are currently worth $15,000 (500 shares x $30).

So, how is this treated for tax purposes? At the time the NSOs are granted, there is no taxable event. However, there are two taxable events that occur both at the exercise of the stock options and the sale of the stock.

Suppose you exercised options on 500 shares of XYZ at $30. At this point, the $20 difference between the exercise price and the original grant price would result in $10,000 taxed as compensation at ordinary income tax rates. If you then decide to hold the stock shares for one year and sell when the stock hits $40, the $10 difference between the exercise price of $30 and the current stock price of $40 would result in $5,000 taxed as a long-term capital gain. See Figure 1.

Restricted Stock Units and Performance Shares

Restricted Stock Units (RSUs) are different from options, in that they represent a promise from your employer to pay a certain number of the company’s shares to you upon the completion of a vesting schedule. Unlike stock options, RSUs are simply awarded to you as compensation and do not need to be purchased. Depending on the company’s plan, you may or may not receive dividend payments on the RSUs prior to vesting.

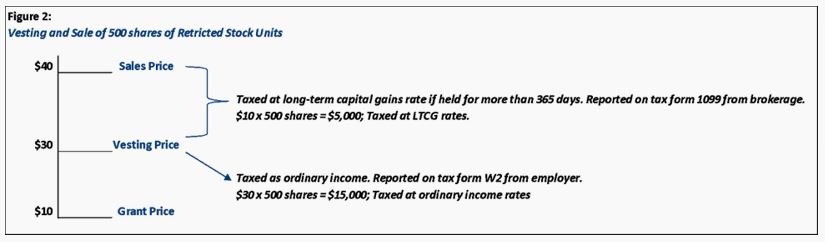

For example, assume your employer promises to award 500 shares of XYZ stock to you upon the completion of three years of employment. At the time of the issuance, the market price of XYZ stock is $10 per share. At the completion of the 3-year vesting schedule, the price of the stock had increased to $30. You would be awarded the 500 shares of XYZ stock valued at $15,000. On the other hand, if the value of the stock dropped to $5 you would receive the 500 shares of stock valued at $2,500.

Performance Shares work similarly to RSUs, but in addition to having a vesting schedule, there is also a performance condition that must be met. This type of grant is usually used to provide an incentive to executives and managers to improve the performance of the company and align them with shareholder interests. Typically, there are two types of performance measures: operational performance (measured by earnings per share or return-on-assets) or market performance (measured by shareholder rate-of-return).

Similar to stock options, there is no taxable event on the initial grant of RSUs and Performance Shares. The units or shares are still subject to certain conditions being met, so the employee has technically not received any value that is certain. Rather, the taxation to the employee will first occur at the end of the specified vesting schedule (in our example three years), and/or the completion of terms in the performance requirements. The actual value received at vesting will be considered compensation and would be subject to ordinary income tax. The future sale of those shares will then be subject to tax on any gain on the sale of the stock, subject to short or long-term capital gain rates depending on the holding period after vesting.

See Figure 2. We assume the initial restricted stock grant price is $10 and the shares vest in three years when the stock price is at $30. The entire value of the RSU award is taxed as ordinary income to the employee based on the fair-market-value of the shares on the vesting date. Any later sale of RSUs or Performance Shares is taxed in the same way as stock options, with long term capital gain rates being available if the shares are held over the one-year period.

Important Considerations

Equity compensation plans are a great financial resource to build long term wealth; however, there are some important considerations to keep in mind.

How much of your financial resources should be tied to your current employer? If the company fails, not only would you lose your salary, but also your stock in the company. Just as with any long-term investment plan, diversification can be a key factor in protecting your balance sheet and mitigating risk. Aim to keep less than 20% of your financial assets in one company.

What is the long-term growth outlook for you company? If your company doesn’t have a history of strong performance, consider negotiating a higher salary in lieu of equity.

When should you sell my stock options or RSUs? Considering your overall tax situation, both now and in the future, can be a major planning opportunity when evaluating the timing of the exercise or sale of your equity compensation. In some cases, it may make sense to wait to sell your equity grants if you are expecting to be in a lower tax bracket in the future or if your company has stock ownership requirements.

Non-qualified Stock Options, Restricted Stock Units, and Performance Shares are just a few types of equity compensation plans that companies offer employees today. It is important to understand how these various plans work. Over time, it is important to consider the tax implications as you get closer to becoming vested. However, tax is not the only important consideration. As the value of the equity you have in your company grows, it is also important to consider how much of your financial assets are tied to the company, whether or not you should continue to hold the stock, and the timing of when you should sell it.