COVID-19 crisis: An update and perspective on the recovery

Key Points:

Stock markets have recovered significantly since March despite bad news about the economy. Stock market volatility has increased recently on concerns of a second wave.

While stocks in aggregate are more expensive, there is still opportunity across the market. When it comes to deciding how much to allocate to stocks now, the better and more strategic approach is to base the decision on an investor’s long-term financial plan.

If evidence of a widespread material second wave begins to surface, stocks will very likely drop. However, stock markets are not likely to go down to March lows. Stock markets could also continue their move much higher once we see a real cyclical recovery in the economy.

To adjust portfolios for what could happen next, Capstone is rebalancing portfolios when markets trends are pointing upward, maintaining an overweight to U.S. large-cap stocks and high-quality bonds, and taking advantage of the market rebound to reduce client portfolio concentration risk when needed.

The constant influx of crisis news amid volatile financial markets and terrible economic data naturally causes us to focus mostly on the negatives. Despite the dire situation and uncertainty we face going forward, we find three big reasons for optimism.

WHAT IS BEHIND The STOCK MARKET RECOVERY?

Stock markets have recovered significantly since March despite bad news about the economy

Over the last several weeks, stocks have rallied to erase most of this year's losses. The optimism in the stock market has been at odds with economic data signaling that the pace of the global economic recovery following the coronavirus pandemic is likely to be slow and uneven. However, there a many things that have contributed to the steep ascent in stocks since the end of March including the slowing spread of the virus; anticipation of the reopening of the economy, early signs of progress on potential drug treatments; investor fear of missing out on the rebound (e.g., investing cash and rebalancing portfolios); and optimism about the technology sector's prospects.

But perhaps the most important contribution has come from the abundant stimulus provided by policy makers around the world and confidence that governments and central banks will take more steps to shield their economies from the worst of the fallout.

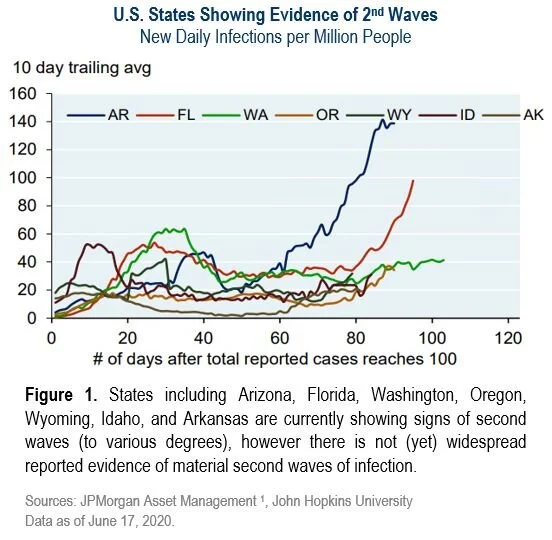

More recently however, stock markets have experienced big down days on emerging signs of a second wave in coronavirus cases in some U.S. states that have begun to reopen their economies. Second wave states are states whose infection rates had fallen, then flatlined, but are now rising again. (See Figure 1.) Regardless of whether these data points are early evidence of material second waves that could prompt the re-imposition of lockdowns in certain states, it is becoming increasingly clear that U.S. Federal Reserve (the Fed) believes that the economic fallout will take more time.

In a recent statement, the Fed projected a prolonged period of unemployment and economic weaknesses. While the Fed has committed to continue supporting the economy until a robust economic rebound occurs, investors could become increasingly concerned that the current government stimulus may run out if the economic malaise continues for much longer. The focus will then turn to whether the Congress will pass another needed stimulus package.

IS NOW A GOOD TIME TO REDUCE MY STOCKS?

While stocks in aggregate are more expensive, there is still opportunity across the market

Stock valuations have tightened significantly after markets staged a stunning comeback; the stock market, in its entirety, is less attractive today than it was in March. This leads to the question of whether an investor should reduce their stock allocation now, perhaps because stocks may have little left to run, especially given the wall of uncertainty ahead. However, under the hood, there is a large dispersion of valuations across the entire stock market. In other words, some sectors and areas of the stock market have recovered much more than others that are still significantly discounted. (See Figure 2.) For long-term investors, there is still a lot of opportunity in the stock market.

Asset allocation decisions should be based on one’s financial plan

Whenever we are asked the question about whether one should decrease (or increase) their portfolio’s stock allocation we answer it by re-visiting their financial plan. That means we evaluate one’s progress toward reaching their long-term goals. Part of the evaluation includes ensuring that one’s current asset allocation is still appropriate to meet the necessary long-term return assumptions built into the plan, without taking on any unnecessary risk. Ultimately, this type of ongoing analysis should be used determine if the amount of stocks that one has in their portfolio is still appropriate.

An alternative approach is to base the stock allocation decision on short-term market conditions and guesses about the future direction of stocks around unknown outcomes of events. Unfortunately, this alternative approach is not enduring and typically results in falling short of one’s return targets over time. The better and more strategic approach is to base the asset allocation decisions on an investor’s long-term financial plan.

WHAT IS THE OUTLOOK FOR THE MARKET AND ECONOMY?

Stock markets will continue to be choppy but are not likely to revisit the March lows

Although stock market volatility has subsided significantly since March, the high degree of uncertainty we still face going forward will likely result in rough waters ahead. Despite a looming U.S. election and rising U.S. tensions, the virus will likely be the main driver of financial markets. If evidence of a widespread material second wave begins to surface, stocks will very likely drop. However, stock markets are not likely to go down to March lows, given the extraordinary amount of economic stimulus being deployed globally.

Additionally, having gone through what is likely the worst of the pandemic, the world should be better prepared to handle a next wave with greater hospital capacity, more widely available personal protective equipment, and best practices that the world is now familiar with to help limit the spread. All of this should (hopefully) result in less restrictive, perhaps more localized lockdown efforts as opposed to more nationwide ones.

Stock markets could also continue their move much higher

As we mentioned earlier, the stock market recovery since March has been tied to various early signs that the worst of the pandemic is over along with significant (ongoing) stimulus support. However, we have yet to see a real cyclical recovery in the economy. Once the economy starts to materially improve, we could see further sharp increases in stocks, particularly those in the sectors and areas of the market that are still beaten down.

Additionally, despite the recovery in stocks so far, expectations are still quite low. There is a lot of pessimism, with lower earnings forecasts, dire economic outlooks, and all-time low investor confidence. When expectations are low, there is room for positive surprises to sustain or push stocks up much higher.

The economy is showing emerging signs of picking up

Broad economic activity remains depressed; however, we are seeing early signs that perhaps the worst effects of lockdown efforts are behind us. In the U.S., the labor market is showing signs that layoffs are slowing, and jobs are being created again.2 Although consumer confidence remains at multi-year lows, there are emerging signs of pickup in consumer spending. (See Figure 3.) While this shows that there has not been a large pickup in economic activity (relative to prior year levels) following recent re-openings, it is reassuring that consumer spending -- the main driver of the U.S. economy, which accounts for more than two-thirds of economic growth -- has seemingly bottomed.

The economy will likely take longer than expected to fully recover

The U.S. economy still has a long way to go to fully recover, with some economists projecting it could take at least two years. While turning off the economy was as easy as flipping a light switch, reopening the economy will be much like using a light dimmer: a far more complex, and therefore, gradual process. Many have written about whether the global economies will experience a “V-shaped” or “U-shaped” recovery, in which these letters potentially resemble the shape of the economic recovery. The reality is that we are likely to experience combination of both, with some parts of the economy recovering more quickly than others. (See Figure 4.) This type of recovery is likely what other countries will experience as well.

The disconnect between the stock market and the economy could converge

It may be hard to understand the current disconnect between the market and economy (i.e., markets rising and economy falling); to us, however, it is not completely surprising. If the past is any indication, markets tend to care more about the direction of economic data rather than the level at which it currently stands. At the moment, we appear to have reached a point where the rate of decline in economic activity has slowed while some activity has started to increase again.

WHAT IS CAPSTONE DOING TO ADJUST MY PORTOLIO FOR WHAT COULD HAPPEN NEXT?

We have been actively analyzing client investment plans as part of our normal ongoing financial planning process. One of the main outcomes of this process is to determine whether the amount of stocks that one has in their portfolio is still appropriate. While it is rare that short-term market movements alone result in a needed strategic asset allocation change, there are occasions when aspects of one’s financial objective and situation changes. If you have recently had a material change to your financial objective or situation, please reach out to us.

In addition to evaluating financial plans, we have been doing the following:

Rebalancing portfolios when markets trends are pointing upward

We continue to actively rebalance portfolios; however recent rebalancing activity has shifted from an opportunistic-investment focus to a risk-management focus. Earlier in the year our disciplined approach to portfolio rebalancing helped to opportunistically position portfolios for a market recovery by trimming from overweight bond positions and adding to stocks that were significantly discounted.

After the recent stock market surge, our rebalancing activity has shifted to risk-management by trimming from now overweight stock positions and adding to bond positions. Bringing portfolios back to their neutral stock and bond asset allocation targets should help to mitigate risk in portfolios from a potential major setback in the stock market if we were to experience a second wave of COVID-19 cases.

Maintaining an overweight to U.S. large-cap stocks

In late-March we increased portfolio allocations to U.S. large-cap stocks. This shift has benefited portfolios so far, and we continue to maintain this overweight. Given their relative strength, U.S. corporations should be more insulated should global stock markets fall again amid this ongoing crisis. Additionally, sturdier large companies will likely be better able to withstand the economic slowdown, particularly if it lasts longer than expected.

We continue to believe that the U.S. economy will be much better positioned for recovery compared to many other major economies abroad. This is due to the unprecedented amount of economic stimulus being injected into the U.S. economy, and the fact that the U.S. already had a relatively stronger economy going into the crisis.

Maintaining an overweight to high-quality bonds

Well before the onset of the pandemic, we positioned portfolio bond allocations to be more defensive against stock market declines by buying high-quality, low-default risk types of bonds such as government, municipal, and investment-grade corporate bonds. These types of bonds have provided much-needed stability to portfolios this year and we expect this protection to continue. Despite the opportunity that still exists in lower-quality corporate bonds that have declined in value and are currently offering higher yields to investors, we continue to maintain our high-quality bond overweight. We still do not believe that now is the right time to go down in quality because of the still elevated potential risks of economic uncertainty and further stock market declines.

We also do not believe now is the right time to shift out of government bonds, despite record-low interest rates. Interest rates will likely stay low for the foreseeable future, so we are not concerned at the moment about bond prices going down. We are as comfortable as ever with the bonds we have in portfolios. These types of bonds should remain good preservers of capital.

Reducing portfolio concentration risk

Capstone portfolios are highly diversified across individual companies, sectors, and countries, and will continue to be managed this way. We often work with clients that either have outside investments or have come to Capstone with concentrated portfolios, most often in individual stocks from prior employers. After the stock market’s recent run-up, there has now been a great opportunity to trim or remove concentrated holdings from portfolios to shift the proceeds toward more diversified risk-based holdings; or rebalance portfolios into bonds; or to fund near-term cash flow needs.

ARE THERE REASONS FOR OPTIMISM AMID ALL THE BAD NEWS?

The COVID-19 pandemic has captured our attention and will likely do so for many more months to come. The constant influx of crisis news amid volatile financial markets and terrible economic data naturally causes us to focus mostly on the negatives. Despite the dire situation and uncertainty we face going forward, we find three big reasons for optimism:

1. Conditions have stopped getting worse

We have reached a point where infection rates have, so far, stopped getting worse in most of the hardest-hit countries. Containment measures have worked, allowing hospitals to better handle the influx of patients and economies to start opening up again. In the U.S. and Europe, the decline in economic conditions is slowing while some economies are already starting to improve. In the U.S., there has been a lot of focus (rightfully so) on the skyrocketing unemployment numbers. (See Figure 5.) Recently however, the numbers have started to come down. More importantly, over 80% of jobless claims are classified as “temporary layoffs” that are likely come back on line.

2. An unprecedented amount of stimulus is supporting economies and markets

Our economic system is resilient and has overcome equally large problems in the past. Key resources and stimulus packages are being developed and will continue to be deployed. So far, we have had a tremendous amount of stimulus from governments and central banks around the world. As of May, the U.S. government and Federal Reserve have committed up to $10 trillion in stimulus. International governments and central banks have combined to contribute another $10 trillion.5 All of this fiscal and monetary stimulus has helped (and should continue to help) limit permanent economic damage and keep financial credit markets working. The worst global economic damage ever is being met with the biggest stimulus measures ever.

3. Worldwide focus on medical solutions

There are thousands of medical science professionals working on treatments and cures; hundreds of companies and entrepreneurs are striving to address the challenge. Scientists have been able to shorten some of the steps-to-market for several of the vaccine candidates. Once a vaccine or viable treatment becomes available, there will likely be a surge in economic growth. Throughout history, we have overcome diseases such as COVID-19, and there is no reason to believe this one will be different.

Despite all the uncertainty, there are still reasons for hope.

We will continue to keep you updated on the evolving situation. Please do not hesitate to reach out to us should you have any questions or concerns. As always, we are here for you.

Sources

¹ https://am.jpmorgan.com/us/en/asset-management/institutional/insights/market-insights/eye-on-the-market/coronavirus-covid-19-research-compilation/#covid2

² https://www.bls.gov/news.release/pdf/empsit.pdf

³ https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/06-08-2020%20-%20The%20bounce_AMV_NI.pdf

⁴ https://advisors.vanguard.com/insights/article/thegreatfallandtheroadtorecovery

⁵ https://www.jpmorgan.com/jpmpdf/1320748651296.pdf