What You Should Know About Annuities

Key Points:

Though the goal for most annuities is simple—to provide income over a certain period—the varying types of annuities and contract terms that are available make the decision process of whether to purchase an annuity a complex matter.

There are significant benefits and drawbacks to annuities that are important to consider, including the tradeoff between guaranteed lifetime income and flexibility.

It is important to factor in your individual circumstances and risk tolerance when purchasing an annuity can make sense, as compared to investing those funds in a diversified portfolio.

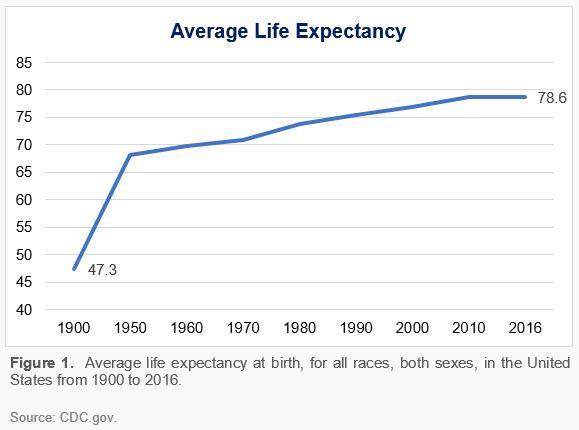

According to the latest study by the Centers for Disease Control and Prevention, from 1900 to 2016, the average lifespan for an individual living in the United States increased from 47 to almost 79 years of age – an increase of 66%.¹ (See Figure 1.) Because of continued major advances in public health and social awareness, people living in the United States and much of the developed world have been able to live much longer. Though these advances have been nothing short of spectacular, one problem this has created is that some people may now outlive their financial assets.

Social Security & Employer Pensions – The Annuity Solution

In a response to a growing epidemic of poverty amongst the elderly, the Roosevelt Administration (in conjunction with the Treasury Department) signed the Old Age and Survivors Disability Insurance Program (OASDI) into law in 1935². A major part of this legislation was the Social Security system. Still a major component of many workers’ retirement benefits today, Social Security is a form of annuity that pays a stream of income each month to an individual over the course of their lifetime. To receive such benefits and preserve the program’s financial viability, individuals and employers must pay a certain percentage of their paycheck into the Social Security system each year while they are working.

Around the time that the OASDI was signed into law, employers also began to offer pension plans, which in exchange for monthly contributions during employment, paid a certain stream of income at retirement. Recently, pension plans have largely been phased out in favor of 401(k) and other Defined Contribution plans due to employer concerns related to the high costs and liabilities of pension plans.

Private Annuities – The Annuity Contract We All Know

As an added solution and a response to the destitution that the Great Depression inflicted on many Americans, the insurance industry experienced a massive demand for private annuity contracts. Individuals could purchase these contracts either in the form of monthly premiums, or via a lump-sum cash deposit. Simply referred to as “annuities” today, these contracts have evolved over time and grown in popularity. Though the goal for most annuities is simple – to provide income over a certain period – the degree to which they can be used in other situations, such as asset protection planning, has grown as well. For example, in certain situations, annuities can receive certain creditor protections that may be desirable for some.

For many consumers, the various types of annuities that are available today, along with the complex terms within each annuity contract, can make the decision-process surrounding an annuity purchase difficult. Being able to understand some of the major benefits and drawbacks of annuities can help an individual in making a sound decision.

Benefits of Annuities

A few of the major benefits that annuities may provide include lifetime income, tax deferral and principal protection.

Lifetime income is a guarantee on certain annuity contracts that provides the policy or contract holder with payments throughout the course of their lifespan. There is no limit to the amount one can contribute to an annuity and thus, no limit to the size of the payments offered. This is a key advantage for individuals with significant amounts of cash available to invest that want to convert that cash into a lifetime income stream.

Another benefit annuities offer is tax deferral. With many annuities, a consumer can contribute money to the annuity and not pay any taxes on the earnings until withdrawal. Like an IRA account or 401(k) plan, the amount contributed has a chance to grow tax-free, allowing for more effective growth.

Principal protection is a feature offered on certain annuity contracts, which guarantees that the value of the annuity never falls below the total amount contributed, or that losses are limited by a certain percentage each year. Though other investment options carry an inherent amount of risk, this feature helps to mitigate that risk and provide a level of security that some people may value.

Our Take on Annuities

Despite the higher expenses, limited flexibility, and limitations that can be associated with annuity contracts, there are important advantages to consider when looking to add an annuity to an investment portfolio, such as unlimited contribution limits and guaranteed income streams. It is important to consider your goals and how an annuity may fit in achieving those goals. It is also important to review all the terms in an annuity contract, as the offerings are so numerous and varied. Everyone’s situation is different, and it is important to factor in your individual circumstances and risk tolerance when deciding if an annuity makes sense for you.

Sources:

¹Centers for Disease Control and Prevention, Life Expectancy

²Social Security Administration, Historical Background And Development Of Social Security

³Annuity.org, Annuities